The yield curve plots the returns on government bonds by maturity, starting from the shortest and going up to the longest ones. The chart is closely watched as it can provide interesting indicators about the investors’ perception of future economic trends.

Usually, the yield curve slopes upward. Short maturities come with lower yields and, as maturities increase, yields rise, too. Unpredictability and risk are the factors behind it. The longer the investment horizon, the higher the likelihood of unexpected developments. Economic trends of the near future are easier to anticipate than those of the very distant future. Therefore, to invest long-term, investors expect a risk premium, meaning a higher yield to reflect the higher risk they take. This turns a “normal” yield curve into an upward slope, with increasing returns on longer investment terms.

It is not the direction alone, but the slope of the upward curve that matters as well. A steep slope, for instance, reflects the investors’ expectations for an acceleration of the economic growth, accompanied by a rising inflation.

However, there are cases, rather rare, where the yield curve ceases to be “normal”. It becomes “inverted”. In other words, it slopes downward, as short maturities offer higher yields than long maturities. It may seem counterintuitive at first, as it appears to contradict the reasoning above, namely that the risk associated to long-term investments is better remunerated.

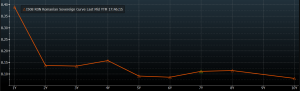

It is the kind of situation currently facing the government bonds market in Romania. After a long period where the yield curve was “normal”, it now starts to invert, as shown in the chart below. What is the meaning of this inversion?

A first question would be: does this curve anticipate the infamous stagflation, much talked about in Romania these days? I don’t think so. The word “stagflation” is made of stagnation and inflation. Indeed, an economic stagnation followed by a recession might produce such an inversion. But not the prospect of inflation. Why would one accept lower yields when expecting the inflation to soar?

So, does the curve inversion predict the start of the recession for the Romanian economy? Particularly since this is the standard interpretation especially in developed economies: yield curve inversion = recession. I do not think that Romania can go into recession in the absence of a powerful external shock. An economic slowdown perhaps, stagnation maybe, but not a significant and lasting economic downturn. Moreover, given the budget’s rigid structure, the huge deficit and the negative impact a recession would have on revenues, a higher budget deficit induced by the recession would force the government to offer higher, instead of lower interest rates.

Of course, the scenario of a recession triggered by an extreme external shock cannot be completely overlooked. But the inverted curve does not reflect extreme scenarios. Investors, in general, have a limited capacity to anticipate extreme scenarios.

So, what option remains? From my perspective, the explanation has to do first with the central bank’s accelerated increase of the interest rate. With the “wait-and-see” attitude towards inflation displayed during the initial months of the year, BNR appeared to open a sure path towards a significant and extended bout of inflation. But the latest BNR board minutes indicates the admission of the initial incorrect evaluation, the presence of signs of economic overheating and the need for a rapid repositioning of the monetary policy.

Such a message entails two consequence that are relevant for investors in long-term bonds. Firstly, the fact that, if BNR keeps adjusting the monetary policy at the same rate, the inflation should rapidly be brought under control. Therefore, an annual yield of 9% on 10 years cannot be justified and represents a rare investment opportunity. Secondly, a policy to increase interest rates reduces the chances of a depreciation of the RON. This means that the FX risk that foreign investors take when buying RON-denominated bonds is low, which is likely to encourage them. Which became apparent at the most recent long-term T-bond auction with significant foreign presence.

To conclude, I think that, in Romania’s case, the yield curve is currently mirroring the credibility of the BNR monetary policy in the fight against inflation. A decisive approach from BNR should maintain the curve inverted for a period of time. Its quick return to “normal” would be a bad sign for the credibility of monetary policy in terms of getting the inflation within the inflation target.

Have a nice weekend!